If I had $1,000: A Guide for Young Investors

Q1 | February 2026

Topic: Wealth Planning

February 26, 2026

Image used with permission: iStock/PhanuwatNandee

Download This Issue

Download this full issue of Nexus Notes QuarterlyIf I had $1,000: A Guide for Young Investors

Q1 | February 2026

As my third anniversary at Nexus approaches, I am making my debut to the Nexus blogosphere. I’ve been fortunate enough to meet many of our clients over the last few years, but if I have not yet had the pleasure, let this be an informal introduction.

In 2023, I joined Nexus as a Client Service Associate and have been working and studying toward my Certified Financial Planning (CFP) designation. As Spring 2026 approaches, so too does my certification once my three years of work experience are completed under the guidance of the Nexus Wealth Planning team.

Personal Finance can be Overwhelming

As someone at the beginning of my career, I know from my own experience how opaque the financial industry can be. It isn’t easy to interpret all the jargon and acronyms, so getting on the right financial track early on can feel more aspirational than realistic for some. With that in mind I’ve created a roadmap for our next generation (NextGen) of investors who find themselves in a similar life stage to me.

You’ve Got an Extra $1,000 – Now What?

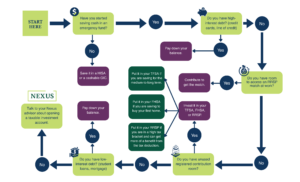

So, let’s imagine that you’ve suddenly come into some extra cash. For simplicity, we’ll say $1,000. This could be a holiday gift, a year-end bonus, or a refund at tax time. Where does a financially savvy NextGen investor put a modest windfall? The answer really depends on the individual’s unique circumstances, but the flow chart below can help you make decisions and illustrates some of the logic the Nexus Wealth Planners use when making recommendations.

Investing Thoughtfully, The Nexus Way

While I’m writing with the young investor in mind, these principles remain largely the same no matter your stage of life. A Nexus Wealth Plan and our recommendations will always be tailored to the individual. However, we consistently prioritize building an emergency fund, paying down high-interest debt, and topping up registered contribution room before we assess other options for your surplus cash. It should be noted that there is more nuance to the discussion when we start talking about larger sums of money. Your advisors should be involved in any discussions that make a more substantial impact on your goals or overall financial picture.

Step One: Build an Emergency Fund

First, we recommend building up a cash reserve for emergencies. With an emergency fund, your longer-term savings can continue to accumulate and grow, yet you still have access to debt-free cash. For example, if you have an unexpected car repair or a hiccup in your regular earned income, tapping into your emergency fund can help preserve your investments and reduce the need for debt. You want your emergency fund to be easily accessible and have no market risk. A High-Interest Savings Account, or a cashable GIC (Guaranteed Investment Certificate) is your best bet. Generally, we recommend a savings goal of 3-6 months of your basic living expenses, which can be built up over time.

Step Two: Reduce High-Interest Debt

Next, we assess whether the investor has any debt with a high-interest rate, such as a credit card, which often charges around 20%. The money you spend on interest payments would be much better allocated to your savings accounts, so we want to pay down that debt as quickly as possible to avoid paying high-interest. If your interest rate is lower, think less than 5%, we tackle that later in the chart.

Step Three: Don’t Miss Out on Free Money

After you’ve tackled high-interest debt, we want you to explore if you can increase your $1,000 with an employer match. Many workplaces offer an RRSP matching program where the employee contributes a certain amount and the employer will match your contribution up to a pre-determined threshold. This is free money(!) and gives you even more bang for your savings buck. If this is not an option, or if all available contribution room to the RRSP is already used up, then we continue on.

Step Four: Choosing the Right Registered Account

Once a NextGen investor comes to the point where a contribution to your tax-sheltered, or registered accounts, is the next best option, the appropriate account type really depends on your individual goals. In general, you’d likely see us prioritize contributions to a TFSA (Tax-Free Savings Account) and then an FHSA (First Home Savings Account) or an RRSP (Registered Retirement Savings Plan).

Our first choice for young investors would be the TFSA because it gives the greatest withdrawal flexibility, especially when you may have multiple competing financial goals in the short term. Second, though an FHSA has very specific withdrawal requirements, it is an excellent new vehicle for your investments if the account and the contribution room are available to you. Lastly, we would recommend contributing to an RRSP because, beyond the tax deferral, a major benefit of the RRSP is the tax deduction. However, this is of most value to you when you are in a high-tax bracket, and the deduction gives you the greatest benefit. Withdrawals from RRSPs are also taxed as income, so it is not the right account if you need withdrawal flexibility in your early working years.

Step Five: When to Invest Instead of Paying Down Debt

Finally, after assessing your registered accounts, we would recommend that you pay down your lower-interest debt, like a student loan or a mortgage. If your expected rate of return, after fees, in a registered account is higher than the interest rate on your debt you are better off mathematically in the long run by investing the $1,000 in your registered accounts. However, don’t ignore the psychological wins. Balance your debt repayment and savings in a way that keeps you motivated, not just math-optimized.

The Long Game: Habits That Matter More Than the $1,000

When working with our NextGen clients, we emphasize the unique benefit of a long time horizon and the power of compounding returns. With that, taking the right steps early sets up future-you for long-term success. If you came to our Wine and Wealth event for our NextGen investors in the fall, or you’ve done a Wealth Plan with us, you know that good financial planning starts with tracking your expenses, setting a budget, building an emergency fund, or paying down debt. Your habits, complemented by the reasoning in the flow chart, can help you get started on your wealth-building journey. If you’re interested in doing a Wealth Plan with the Nexus team, please send us an email.